Gold - The Pro's Way, The Boom, And My Least Favorite

Oct 25, 2025

What's Driving This Boom - Part 1:

Gold is having a moment—quietly. Year-to-date, measured in U.S. dollars, the metal has outpaced major equity markets, not with meme-stock theatrics but with a steady grind higher. Storage facilities report a brisk business from the ultra-wealthy, benchmark prices have printed records across most major currencies, and the standard 400-ounce bar has crossed the million-dollar mark.

Two features of this rally stand out. First, gold’s traditional tether to “real” (inflation-adjusted) U.S. interest rates has slackened. For decades, falling real yields were the spark in the tinder; recently, that link has looked muted. Second, the usual high-beta travelers—silver and gold miners—haven’t kept pace. Silver has repeatedly knocked on, but not broken through, the $30/oz door. Miners, notorious for destroying capital in long cycles, continue to lag their underlying commodity.

So what’s changed?

Gold’s Job Description: Fallback Money

Strip away the lore and gold is a simple instrument: a bearer asset that requires no one else’s promise to hold value. It is durable, fungible, divisible, and—crucially—its supply grows slowly. Those properties have made it a serviceable form of “physical money” for millennia.

Modern money is a social technology; it evolves because convenience and credit are powerful. That’s why we don’t settle our salaries in coins. But when confidence in a given system frays—whether through inflation, capital controls, sanctions, or institutional failure—gold’s archaic inconveniences start to look like features. This is not an end-times argument. It’s a practical one: in countries facing disorder or sanctions, gold serves as portable, system-agnostic savings.

Why Central Banks Moved First

This cycle began not with retail buying or ETF flows, but with central banks. That alone is telling. Consider the last great nadir for official gold—Britain’s sale of roughly half its reserves between 1999 and 2002, in the afterglow of the Cold War and on the cusp of the euro’s birth. It was an age of institutional faith and monetary experimentation.

Today’s setting is different. Geopolitical blocs are hardening. Sanctions have become an explicit policy tool. The dollar’s hegemony isn’t collapsing, but access risk has become a line item for nations outside the U.S. orbit. If you fear being cut off from the dollar plumbing, you accumulate assets that clear outside it. That list is short. Gold sits near the top.

What It Means for Portfolios

Treat gold less like a “trade” and more like insurance. It is the rare asset owned consistently by the most sophisticated balance sheets on earth—central banks—even at the bottom of cycles. That doesn’t mean its cousins deserve the same treatment. Silver, miners, and related cyclicals can be excellent vehicles in manias, but they are fair-weather friends. Capture the sun; don’t forget that winter returns.

How to Own Gold: Vehicles, Risks, and a Working Playbook (Part 2)

Collectible coins in remote vaults make for great stories, but they don’t suit every investor. If you go that route, education is non-negotiable. The coin market is rife with premiums over spot, opaque markups, and liquidity frictions that often surface only when you try to sell. Custody is another issue: vaulting with a third party concentrates operational risk precisely when you may need access most. If you insist on coins, know the market, take possession, and store them securely. Usually there’s no problem—until it’s time to sell and get your money. Be careful before investing in coins: learn the market thoroughly. If you haven’t attended precious-metals trade shows or studied the major coin types, my view is to avoid this segment altogether. And remember those gold-bug TV ads—someone is paying for them. Most are selling coins, and it’s often investors footing the bill.

Investors have cleaner options:

1) Unlevered ETFs (e.g., GLD)

What it is: Exchange-traded exposure that tracks bullion.

Why it works: High liquidity, tight spreads, easy entry/exit during market hours.

Trade-offs: Management fees and minor tracking slippage versus spot; you own shares, not bars.

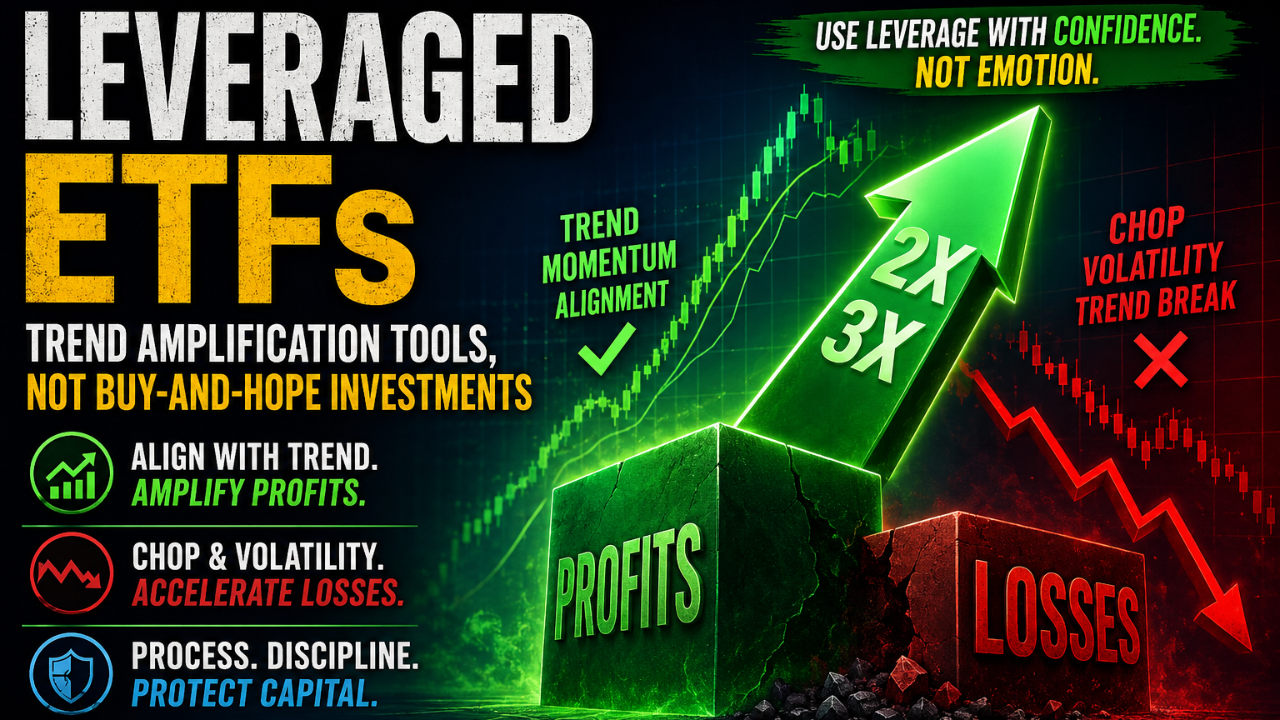

2) Leveraged ETFs (e.g., UGL)

What it is: Products targeting 2× daily moves in gold.

Why it works: Amplifies upside without using margin directly.

Trade-offs: Daily rebalancing and path dependency; can erode value in choppy markets. Best suited to tacticians, not long-term holders.

3) Options on GLD (or on Leveraged ETFs)

What it is: Calls/puts to express directional or volatility views with defined capital at risk.

Why it works: Asymmetric payoff; can “turbocharge” exposure.

Trade-offs: Time decay, strike/tenor selection, and higher complexity. Options magnify both skill and error.

4) Futures on Gold (GC)

What it is: Institutional-grade leverage (roughly 20:1) via standardized contracts.

Why it works: Deep liquidity, efficient capital usage, 24-hour trading.

Trade-offs: Mark-to-market, margin calls, and swift P&L swings. Futures reward discipline and experience; they punish the rest.

For example, a multi-contract, multi-month gold futures stance during a sustained 2025 up-leg could have generated triple-digit percentage returns on capital. If you had invested $1,000,000 in January 2025 in the futures market (bought 33 gold contracts) by October, that account would be worth approx $4,700,000. That's a nice gain. The same structure in a whipsaw could incinerate equity just as fast. The point isn’t the headline number; it’s that futures are a professional’s tool that can really take advantage of moves like we are seeing on Gold. The commodities market often will see a derivative like Gold. You just have to have the capital set aside and waiting for the next Gold market to pop up.

That's if you only bought 33 contracts. What if you had the capital to buy 50 or 100 contracts? Like I said earlier, I can't stress enough that futures is the most risky option for growth and must be handled by a professional who knows what their really doing.

A Practical Framework

-

Define the role. Treat base gold exposure as portfolio insurance—size it accordingly and rebalance.

-

Separate vehicles by mission. Core: unlevered ETFs. Tactical: options and leveraged ETFs. Professional/high-skill: futures.

-

Obsess over liquidity and access. If you can’t press “sell” during market hours and settle promptly, ask why.

-

Respect the cycle. Gold’s satellites (silver, miners, leverage) shine in momentum phases and fade in chop. Harvest gains; don’t annualize outliers.

Bottom Line

Coins and distant vaults cede control when control matters most. For most investors seeking exposure to the monetary hedge, ETFs provide simplicity and liquidity. For those with the toolkit and temperament, options and futures introduce leverage and timing—magnifying both opportunity and risk. In all cases, gold demands clarity of purpose: insurance first, speculation second. I hope you can see why I don't really care much for coins. I think they're nice to have as a collection, but for investments engineered for growth, I prefer the ETFs, Options, and Futures over the coins.